Posted by zerosizedweasle 10/27/2025

Same reason why seemingly every CEO on the planet is making hand wavy statements about how their company is leading with AI and it will revolutionize their industry, and yet almost nobody is willing to break out this amazing stuff in their P&L. Funny how that works.

https://www.channelfutures.com/cloud/amazon-com-breaks-out-a...

By 2015 they were trying to hide how much of the group growth and profits were largely contributed by just AWS , i.e. they were hiding the e-commerce margins .

Without AWS and subscriptions, Amazon is quite an unprofitable company.

Both overall growth and margin driven by AWS(and prime) while E-commerce revenue remains outsized because they count GMV as revenue which is iffy even when they own the merchandise, but being largely a marketplace these days GMV is very misleading metric.

It would be like Stripe decided to count their revenue as $1.4T the amount they processed this year as revenue rather than $10-20B they actually got after paying the banks, merchants , VISA etc . This 20B is not profit either just the pie from which salaries cloud costs etc have to be paid to get to actual profit.

The inverse true now with AWS. Lots of press about analysis on how AWS is in “last place” on AI and while AWS leadership has been doing a lot of hand waving to say they’re not, it’s a pretty safe bet this week’s earnings call won’t have any hard financial numbers to counter press that they’re way behind.

In my experience - and I’ve run comparisons against the various models for projects (consulting) - their in house Nova models usually give me the best results on the spectrum of speed/quality/cost I need for a given project.

"How Microsoft has managed to avoid disclosing such basic details is baffling. The company in its financial reports identifies OpenAl as an equity-method investment. That means OpenAl, by definition, is a related party of Microsoft under the accounting rules. Microsoft, however, doesn't identify OpenAl in its financial reports as a related party, and doesn't say anything about its transactions with OpenAl in its related-party disclosures."

26.5 Common related party transactions

In order to comply with the related party disclosure requirements, a reporting entity must identify all of its transactions with related parties.[…]

26.5.1 Disclosure of related party equity method investments

Equity method investees are, by definition, related parties of the equity holder.

Equity accounted for investments imply it's treated as one and the same as the business, the individual entries will be included with the rest of the entries related to the business being reported on. Related parties are considered external and are basically reported "at arms length". This still doesn't necessarily mean they're providing you with the consolidated results to make matters more confusing.

Separately, They're required to report intercompany transactions with related parties (specific meaning) as there is a lack of visibility on the innerworkings of that related party business (it's external and not included) and the potential conflict of interest exists as they're related and could be used to skew the ratios/reporting of the reported entities results.

1) OpenAI is an “associate” of Microsoft in the IAS 28 sense (which is the reason why it accounts for the investment using the equity method).

2) OpenAI is a related entity to Microsoft in the IAS 24 sense because of (1)

If you disagree with the points above how does that fit with the relevant standards?

———

For what it’s worth ChatGPT tells me the following:

If Microsoft has significant influence over OpenAI (as implied by equity-method accounting), then:

OpenAI is a related party of Microsoft; and

Microsoft must disclose the nature of the relationship and any material transactions between them (e.g., cloud services, licensing, revenue sharing).

———

IAS 24 - Related Party Disclosures

https://www.ifrs.org/content/dam/ifrs/publications/pdf-stand...

A related party is a person or entity that is related to the entity that is preparing its financial statements (in this Standard referred to as the 'reporting entity').

[…]

(b) An entity is related to a reporting entity if any of the following conditions applies:[…] (ii) One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

[…]

A related party transaction is a transfer of resources, services or obligations between a reporting entity and a related party, regardless of whether a price is charged.

—-

IAS 28 - Investments in Associates and Joint Ventures

https://www.ifrs.org/content/dam/ifrs/publications/pdf-stand...

The following terms are used in this Standard with the meanings specified:

An associate is an entity over which the investor has significant influence.

[…]

An entity with joint control of, or significant influence over, an investee shall account for its investment in an associate or a joint venture using the equity method except when that investment qualifies for exemption in accordance with paragraphs 17-19.

———

Edit: I wrote about IRFS below but US GAAP seems similar. What are the “specific definitions” you mention?

https://www.ey.com/content/dam/ey-unified-site/ey-com/en-us/...

An investor and its equity method investee are considered related parties under ASC 850 and should disclose material intra-entity transactions as related-party transactions.

https://arch.bdo.com/getContentAsset/b40b6cee-4d4f-4182-bf43...

DISCLOSURE REQUIREMENTS

Related-party transactions

An equity method investment and an investment accounted for using the fair value option are related parties to the investor, as defined in ASC 850. The investor must provide disclosures about related-party transactions with such entities, including:

The nature of the relationship

A description of transactions, including the amounts

Amounts due to or from the investee.

No this is wrong.

You wrote “Related party in IFRS isn't what you think it is”- but you have not commented on the IFRS definition of related party that I quoted above (and repeat below). Are you thinking of a different IFRS definition?

“An entity is related to a reporting entity if any of the following conditions applies:[…] One entity is an associate or joint venture of the other entity […]”

As I say it's been a while for me. I've given chatgpts reply to your prior point. They've explained it better.

Equity-method accounting does not automatically mean the investee (OpenAI) is a “related party” under U.S. GAAP (ASC 850) unless there is control or common control, or one party can significantly influence operating or financial policies of the other in both directions.

In this case:

Microsoft applies the equity method because it has significant influence over OpenAI, but OpenAI does not have reciprocal influence over Microsoft.

Therefore, OpenAI is not a related party of Microsoft under GAAP.

Microsoft may disclose the nature of the investment and transactions (e.g., Azure hosting, licensing), but not as related-party disclosures—they appear in other sections (e.g., “Investments” or “Revenue from strategic partners”).

In short: → Equity method ≠ related party. → Disclosure still required, but not under related-party rules.

I don’t understand what’s “this” that has nothing to do with related parties.

Your first comment “If its equity accounted it won't be considered a related party as far as I understand. Related party in IFRS isnt what you think it is.” and your second comment “It's not a related party that's the point.” were about what is a “related party” and about nothing else!

You write that “Microsoft applies the equity method because it has significant influence over OpenAI”.

According to IFRS “An associate is an entity over which the investor has significant influence.”

That makes an OpenAI an associate of Microsoft given your previous claim.

Agree or disagree?

According to IFRS “An entity is related to a reporting entity if […] One entity is an associate or joint venture of the other entity”.

In this case one entity is an associate to the other. It doesn’t give to any particular “entity” in that definition the “reporting” role - it says just “one” and “the other”.

That makes OpenAI a related entity to Microsoft if Microsoft has significant influence on OpenAI.

https://www.ifrs.org/content/dam/ifrs/supporting-implementat...

IFRS® Foundation — Supporting Material for the IFRS for SMEs Standard

Module 33 — Related Party Disclosures

——

Ex 4 Parent entity […] has significant influence over associates 1 and 2.

For Parent's separate financial statements […] associates 1, 2 […] are related parties (see paragraph 33.2(b)(i) and (ii)). […]

——

Ex 13 Entity S has significant influence over Entity T. […]

Entity T is an associate of Entity S. Entities S and T are related parties (see paragraph 33.2(b)(ii)). […]

——

In the previous example, set Entity S = Microsoft and Entity T = OpenAI :

Premise: Microsoft has significant influence over OpenAI.

Conclusion: OpenAI is an associate of Microsoft. Microsoft and OpenAI are related parties (see paragraph 33.2(b)(ii)).

Under U.S. GAAP (ASC 850), however, the definition is narrower. “Related parties” include affiliates, principal owners, management, and members of their immediate families—but associates accounted for under the equity method are not automatically treated as related parties unless reciprocal influence or common control exists.

So:

IFRS → associates are always related parties (disclosure under IAS 24.9(b)).

U.S. GAAP → equity-method investees are not necessarily related parties unless additional factors apply.

Microsoft reports under U.S. GAAP, not IFRS, so OpenAI is not a related party in Microsoft’s filings. Disclosures still occur in “Investments” or “Strategic Partnerships,” not under “Related Party Transactions.”

Ok, just for the record you started saying that it wasn't so, talking explicitly about what are related parties in IFRS: https://news.ycombinator.com/item?id=45720653

> Under U.S. GAAP (ASC 850), however, the definition is narrower. [...] associates accounted for under the equity method are not automatically treated as related parties unless reciprocal influence or common control exists.

Is that definition written anywhere?

According to the glossary in ASC 850:

"Related parties include: [...] b Entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of Section 825-10-15, to be accounted for by the equity method by the investing entity"

It says nothing about "reciprocal influence or common control" - only that investments would be required to be accounted for by the equity method. And that's a question of "significant influence".

If Microsoft has "significant influence" on OpenAI (does it?) and is required to account for its investment in OpenAI using the equity method (is it?) then I don't see why it wouldn't be a related party according to ASC 850.

Now, if it doesn't have "significant influence" and is not required to account for its investment using the equity method then it's not an "associate" under IFRS either.

So it seems that if it's an IAS 24 related party it's also an ASC 850 related party. (At least until you provide some evidence for those reciprocal influence requirements you mention.)

A while back there was a big fuss because executives were caught not paying tax on the fair market value of extra perks they were getting like use of the corporate jet on the weekends for trips to the beach house. Anything that’s not purely a business expense is considered compensation and is taxable.

Feels somewhat prescient.

There are many legitimate reasons to not disclose an investment on your balance sheet:

- materiality: immaterial compared to overall position

- classification: research-phase or contingent on future event

- control & ownership: if you don't have significant control or ownership

- off-balance sheet arrangements: SPVs, JVs, lease agreements that don't meet consolidation criteria (disclosed in notes, but not recognized as assets or liabilities due to limited exposure)

- strategy or confidentiality: minimize visibility to protect competitive information or negotiations; must still comply with disclosure rules so details might appear in aggregated or summarized form

- regulatory or accounting policy differences: IFRS vs. US GAAP have different recognition and measurement bases

- held-for-trading or short-term nature: e.g. marketable securities might be short-term trading assets so would be grouped together in a single line item, rather than disclosed separately

That's why some analysts ignore most company-provided metrics and just focus on cash-flow. You need inside and outside of the house fudgers to mess with that metric.

Both are true in many cases. But to the extent companies are making major investments that are strategically correct but won’t make money for years, it’s still the right move to hide stuff in financial statements.

Markets don’t reward long term investments. Everything has to be short term, and if it’s not paying off instantly, short term investors get no value and want it stopped.

Net result: lots of PR about AI, but almost every company is incentivized to downplay it financially.

The AI investment bubble is almost entirely about making long-term, extremely expensive investments. That's what the gigantic datacenter build-out is about, not short-term investments and short-term returns. They're telling everybody, persistently, that they're making huge long-term bets, and the market is rewarding them like crazy. See: Oracle's run due to long-term bets on AI (it's certainly not short-term results causing the stock to do that, their short-term growth has been mediocre).

Amazon for two decades repeatedly told investors they were making extremely expensive, long-term investments in build-out (eg their fulfillment build-out era), where the primary payoff would be far into the future. The market bought into the long-term on the basis that it was attached to Bezos at the center (that he'd be there to deliver that long-term result). The same is true about Elon Musk with Tesla: they have endlessly made outlandish long-term proclamation to drive their stock. Tesla: robot super business, self-driving taxi business, et al - these are 10-20-30 year long-term claims by Tesla and the market has aggressively rewarded it. That's because they think Musk will/might be there to guide it to actuality. In most cases investors don't buy in because they know the CEO & team won't be around even seven years from now.

Markets (investors) reward long-term if they can be made to believe in the long-term. The issue is that most companies are not believable on long-term statements, they don't have a leadership that will be around for any long-term delivery. Buffett, Bezos, Musk, Zuckerberg were/are long-term attachments so the market has been willing to buy in on various long-term bets.

The AI bubble is far from that. Companies are spending tons on GPUs that have limited lifespan, building models that have limited lifespan, using algorithms that are all basically the same, in a space where someone can dump a “good enough” open source model on the market and blow up your business overnight. There’s very little lasting value in what’s being built and the “we’re investing for the long term” arguments don’t hold much water. It’s like saying you’re investing in real estate but then you keep tearing down the building and rebuilding it every 18 months. That just doesn’t work.

There might be some longer term fungible value from some of the baseline infrastructure investments (data centers, electrical upgrades) but those are undifferentiated and highly fungible.

There are parallels here of folks getting so caught up in the hype that they forgot business fundamentals. Everytime folks say “but this is different” and every time it’s not.

But the phrase "this time" requires a lot of hand-waving. The current generation of models is obviously a bubble, which means that businesses based on them are also participants in a bubble. The market seems to be pricing in various unspecified future miracles. Given the history of AI to date, the miracles needed to justify current valuations might arrive next week, next year, or 30 years from now.

They will arrive, though. That part is no longer up for debate by anyone who's been paying attention since AlphaGo, never mind Vaswani.

It's more of a question if it will ever actually be profitable or marketable without subsidizing most of the cost of running it.

We're seeing the same with streaming services right now. 5-10 years ago, everyone thought they needed their own streaming service and heavily invested into building one and acquiring licenses or producing content for it. Now we're seeing the part where they are trying to make it profitable by raising prices/adding ads or both.

I'm not sure if OpenAI will ever be able to just run by themselves. Without major outside investments to subsidize the cost of actually having users use their services.

IANAA so I don't know how true that is. Just wanting to point out that I don't think you're responding to the key point of the article.

They also had tech sharing valid until the OpenAI board declares 'AGI'.

That seems like a really bad deal. And that was probably at the time when Microsoft had the most leverage to make a deal. Their subsequent deals would make sense to be worse.

As far as I know, they have not disclosed it. If you have more information about something concrete regarding ownership, I'd love to hear it. Maybe I haven't understood everything that was stated.

In the end, whatever Microsoft has is probably less valuable than a sizable ownership chunk that most people seem to assume.

I imagine a lot of people are investing in Microsoft as a proxy to OpenAI. Those people are set to be disappointed.

If Microsoft were just Windows, Teams, Azure, Bing and whatever it is, Microsoft would actually feel like a competitor for firms like Canonical or Red Hat or SUSE which happens to be big but nothing special relative to the others, whereas it now, with with this very public service feels like a behemoth.

Although I don’t particularly like their cloud services they are undeniably an important part of Microsoft’s business. (And they also own a large chunk of the gaming industry nowadays).

They’re shuttering half their studios, cancelling half their games, and firing game devs by the thousands as they hand halo over to PlayStation lol. You’re technically right but they clearly aren’t taking that part of their business seriously anymore. IIRC Gamepass has plateaued on subscribers for years now even prior to their very aggressive price hikes over the last 18 months.

I saw an article the other day that said Microsoft is telling developers they have to have a 30% return on their games, which is almost double the industry standard. That’s just absurd.

Edit: worth mentioning that you have people openly speculating at this point that they might not even make another Xbox. I’m not quite in that camp, but I also think it is a distinct possibility given the back slide they are clearly in right own when it comes to gaming. Fun fact: It’s been 4 console cycles, almost 25 years, since we saw a major player drop out.

I did hear the speculation about Xbox as well and I hope it's not true. I quite like the Xbox as a console (Series X was the first one I bought, used to be on PlayStation before that). Competition is good for the console space, and Nintendo and PlayStation aren't really competitors IMO. The audience for Switch and PS/Xbox isn't the same.

They kind of took it from Apple to begin with. We almost had Halo on the iMac before Microsoft acquired Bungie [1].

Suddenly Microsoft has gone from being some software to being everywhere. I know that Azure is huge, but you don't see Azure.

Windows competitors are OSX (and the very good Apple hardware), Linux (which thanks to Valve is gaining users at an increased rate).

Teams competes against Slack/Discord

Azure competes against AWS/GCP.

Bing "competes" against Google Search

While they do have a share of each (and a big share of the desktop) they don't really have anywhere they can grow, they've filled their existing niches and are competing with other equally sized companies in all of them.

So spaffing some cash on AI on the off chance it pays off down the line might look smart.

Hell if AI does pay off then they look good and if it doesn't, it'll look bad for everyone who invested and they can at least shrug off the cash hit.

Now that OpenAI is starting to talk about ads and allowing "erotic" content, I feel more comfortable in my prediction that not only have OpenAI never turned a profit, they never will. They will be consumed by Microsoft or crash the market so hard it's not even funny. The technology will survive, and it will be useful, but OpenAI as a company is done.

Three generations of Twitter leadership couldn’t make ads on that platform profitable and that exposes far more useful user specific information than ChatGPT.

The hubris is incredible.

More and more OpenAI is drawing parallels to the Danish scandal of IT Factory. Self-proclaimed world leading innovation and technology in the front, financial sorcery in the back.

It's a giant money pit, funding a bunch of people who are not long off the crypto grift train if they are at all.

Like, where is this tech headed? Is it always going to be something that can only be run economically off shared hardware in a data center or is the day I can run a “near frontier model” on consumer grade hardware just around the corner? Is it always going to be trained and refined by massive centralized powers or will we someday soon be able to join a peer 2 peer training clan ran by denizens of 4chan?

This stuff is so overhyped and yet so under hyped at the same time. I can’t really wrap my head around it.

perfectly stated, I had to play a lot with some models to get a better picture of how they work and their limitations, before that all the articles I read about them were either "LLMs are the greatest thing ever, totally perfect and made me a 100x engineer" or "LLMs are complete BS and don't provide any value"

I do think we can build great products on top of them, but the way they're being sold implies we'll need no more new product because a chat interface w/ some tool calling is all you'll ever need.

I suspect it is, in fact. But you can also see why a bunch of very very large, overinvested companies would have incentives to try to make sure it isn't. So it's going to be interesting.

Your last statement: are you implying that the AI-bubble is perhaps an attempt at building out more cryptocurrency mining outfits?

But specifically at least one of these people — Sam Altman —- is not, IMO, off the crypto grift train, because he's still chairman of Worldcoin, which strikes me (and more importantly strikes regulators around the world [0]) as a pretty shoddy operation (not to mention creepy and weird).

[0] https://en.wikipedia.org/wiki/World_(blockchain)#Legal_and_r...

There is much more manipulation potential with LLMs than typical ads. I am worried. It gets more and more difficult to distinct ads and the neutral information.

They should've made so much money on direct response and yet somehow they messed it all up.

Just like they should have been a few times as large in terms of users, but they executed really, really badly.

So I'm not sure Twitters failures imply anything about OpenAIs prospects.

> There’s a famous Sam Altman interview from 2019 in which he explained OpenAI’s revenue model [1] :

>> The honest answer is we have no idea. We have never made any revenue. We have no current plans to make revenue. We have no idea how we may one day generate revenue. We have made a soft promise to investors that once we’ve built this sort of generally intelligent system, basically, we will ask it to figure out a way to generate an investment return for you. [audience laughter] It sounds like an episode of Silicon Valley, it really does, I get it. You can laugh, it’s all right. But it is what I actually believe is going to happen.

> It really is the greatest business plan in the history of capitalism: “We will create God and then ask it for money.” Perfect in its simplicity. As a connoisseur of financial shenanigans, I of course have my own hopes for what the artificial superintelligence will come up with. “I know what every stock price will be tomorrow, so let’s get to day-trading,” would be a good one. “I can tell people what stocks to buy, so let’s get to pump-and-dumping.” “I can destroy any company, so let’s get to short selling.” “I know what every corporate executive is thinking about, so let’s get to insider trading.” That sort of thing. As a matter of science fiction it seems pretty trivial for an omniscient superintelligence to find cool ways make money. “Charge retail customers $20 per month to access the superintelligence,” what, no, obviously that’s not the answer.

> On a pure science-fiction suspension-of-disbelief basis, this business plan is perfect and should not need any updating until they finish building the superintelligent AI. Paying one billion dollars for a 0.2% stake in whatever God comes up with is a good trade. But in the six years since announcing this perfect business plan, Sam Altman has learned [2] that it will cost at least a few trillion dollars to build the super-AI, and it turns out that the supply of science-fiction-suspension-of-disbelief capital is really quite large but not trillions of dollars.

> [1] At about 31:49 in the video. A bit later he approvingly cites the South Park “underpants gnome” meme.

> [2] Perhaps a better word is “decided.” I wrote the other day about Altman’s above-consensus capital spending plans: “'The deals have surprised some competitors who have far more modest projections of their computing costs,’ because he is better at this than they are. If you go around saying ‘I am going to build transformative AI efficiently,’ how transformative can it be? If you go around saying ‘I am going to need 1,000 new nuclear plants to build my product,’ everyone knows that it will be a big deal.”

Not sure if increased availability of LLM porn or the gradual erosion of LLMs with ads and sponsored content would be the greater evil on a societal level. Neither is particularly great. But they will certainly drive shareholder value

A quick search seems to indicate that the porn industry has a $100B in revenue per year, 20% of which is from subscriptions. If OpenAI consumed the entire global market for subscriptions, $20B, would that cover their yearly operational cost?

I'm curious what you're referring to here. Did Sam Altman tweet something about this?

So the math is probably harder than it seems.

The exception might be Azure with their LLM services.

There's a mechanism here similar to a Laffer Curve: Charge too much, they lose; charge too little, they lose. OAI needs to strike a delicate balance vs. surging low-cost competition.

Profit is what you have when you have no confidence in how to reinvest what you earn already.

Expect lots of hand wavy “non-GAAP” numbers pushed by leadership trying to gloss over their failed AI investments.

That’s earnings call speak for “If you ignore the pile of your money we lost with bad AI investment decisions, we’ve had a good quarter. Moving on…”

Plus, of course, if OpenAI makes money, that's also good for them.

https://www.cnbc.com/2025/10/23/trump-white-house-east-wing-...

Whether you want to hide it and ignore the history and praise the ballroom, you alternatively omit the demolish part. Propaganda works for both ways.

It is obvious that demolishing is the first step in new construction, and has been done before to the White House. You can't give all the context in a single sentence. You can avoid bias or wording that attempts to sway the audience (propaganda).

There is no praise or value judgement on the ballroom. The neutral PoV statement is "Microsoft donated to a new ball room for the White House east wing."

----

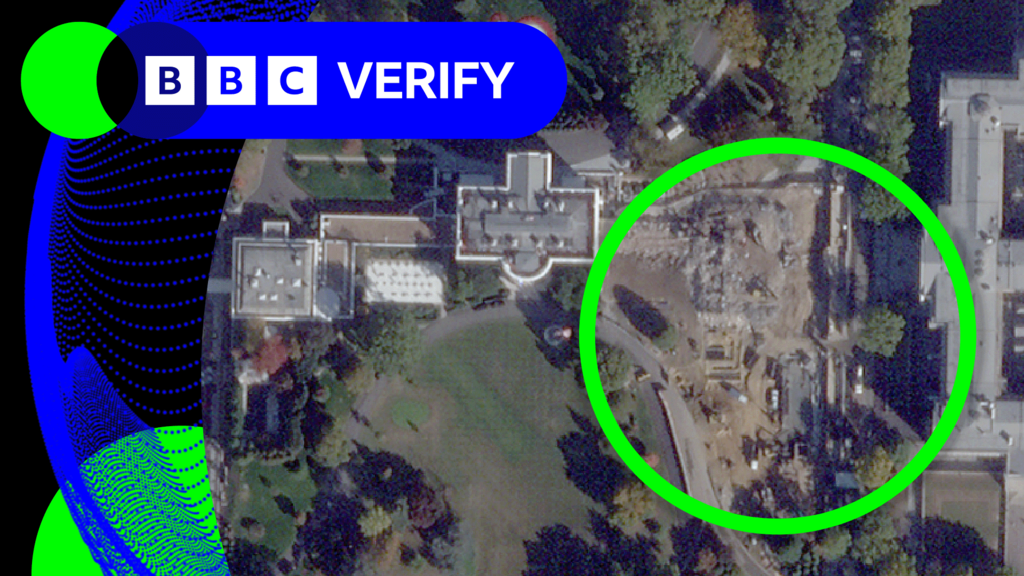

Picture of the East wing today:

https://ichef.bbci.co.uk/ace/standard/1024/cpsprodpb/2089/li...

----

This isn't hard.

I mean, it would have been possible to examine the birthday letters of Myhrvold and Trump and a couple of Trump quotations to put the financing into context.

{kind=link}